Chief executive’s report

Financial performance

|

| Johann Vorster |

During the year under review, South African consumers increasingly had to deal with a weak rand, rising interest rates and high food inflation, which were further impacted upon industrial actions referred to in the Chairman’s Review.

Producers were equally hard hit with increasingly high input cost pressures such as fuel, electricity and feed cost.

For Clover, these constraints impacted on the business as follows:- Costs: We experienced strong overall inflationary cost pressures, especially on packaging and ingredient costs (which are dollar based). In addition, we increased the price we pay for raw milk to ensure on-farm sustainability. These cost increases could not immediately be recovered due to a very constrained trading environment and weakened discretionary consumer spend which necessitated a gradual price increase strategy.

- Lower sales volumes as a result of further selling price increases;

- The erosion of sales volumes due to rising inflation, especially in the non-alcoholic beverages segment; and

- A milk shortage during the winter following Clover’s rebalancing of its milk purchasing agreements in preparation for its exit from supplying raw milk at cost to Danone Southern Africa on 1 January 2015.

Revenue increased by 8,9% to R8 530 million from R7 833 million, whilst operating profit was lower at R282,3 million from R371,6 million in the prior year, representing a contraction of 24,0% for the year under review. Operating margin decreased from the 4,7% reported in the prior year to 3,3%. (The prior year numbers were restated as explained in the Chief Financial Officer’s report).

The net effect was a decrease in earnings per share of 30,8 cents, down 23,1% and headline earnings per share of 17,2 cents, some 14,3% lower than the comparative year.

In order to address the substantial costs pressures on raw milk prices, Clover increased its average price paid to producers by 5,29% from 1 February 2014 and a further 9,53% from 1 March 2014.

Clover’s Margin on Material (MOM) for the dairy fluids product group (mostly UHT and fresh milk which make up the bulk of its raw milk usage) has weakened as a result of Clover’s strategy to gradually recover farm gate milk price and packaging cost increases in the prevailing environment to minimise market share losses in the process. The UHT and fresh milk market conditions during the second half of the year required a cautious approach to selling price increases.

Although not unexpected, the tough economic cycle proved an acid test for Clover’s strategy to exit bulk commodity markets to invest in and focus on branded and value-added products.

It therefore provides me some gratification to report that the new products and platforms introduced during the prior financial year proved the mainstay in Clover’s portfolio during the reporting period.

More information on the performance of each segment is provided later on this report, under Brand Strength and Perfor-mance and in the Chief Financial Officer’s report.

It is therefore imperative that we continue to differentiate ourselves, entrench our brands as the number one or two contenders in the segment and grow the market share of our products in the years to come.

Manufactured capital

New products and platforms introduced during the year under review:- Extended shelf life ("ESL") fresh milk with 18 days shelf life compared to the industry standard of 12 days;

- Prisma packaging for UHT (long life) milk and Tropika fruit juice blend;

- 30 days shelf-life ultra-pasteurised (UP) milk;

- 2 litre carton packaging for the Krush and Tropika brands;

- New formula for Danao in a Tetra Top packaging;

- New processed cheese platform (individually wrapped slices); and

- Clover Amasi (maas).

Corporate activity

As pointed out by the Chairman in his report, some R273,6 million of capex projects have been approved in the year under review of which the bulk has been completed. This excludes the acquisition of Dairybelle (Pty) Limited’s yoghurt and UHT business for an aggregate amount of approximately R200 million which is still pending Competition Commission approval and the last of the Project Cielo Blu spending, .

Projects for the year included:- New Butro platform (better spread ability);

- New 200 ml Tetra Prisma packaging for Tropika;

- Integration and optimisation of Doornkloof factory (Clover Waters);

- Relocation of current Manhattan Iced Tea manufacturing to Inhle;

- Launch of Manhattan Iced Tea in a can; and

- The Real Beverages Company manufacturing integration into Clover’s Parow facility.

Dairybelle has a meaningful presence in the yoghurt market. In addition, the location of its UHT milk production facilities in the Western Cape will provide us with an excellent footprint to improve efficiencies through the more effective utilisation of Clover’s raw milk supply in the region.

We expect that the acquisition will take effect later on in the current financial year, once the suspensive conditions have been fulfilled.

In March this year, Clover entered into a joint venture with Futurelife to jointly launch a new range of functional foods as part of its product expansion plans. In terms of this agreement, Clover will be responsible for the production, sales, distribution and merchandising of these products, leveraging its expertise in dairy and nutrition, supported by its iconic brand. Futurelife will bring its expertise in cereals and functional foods to the table. Futurelife is the fastest growing cereals brand in the country and already sells more product locally than some of South Africa’s most traditional breakfast cereals.

It therefore provides me some gratification to report that the new products and platforms introduced during the prior financial year proved the mainstay in Clover’s portfolio during the reporting period.

Intellectual capital

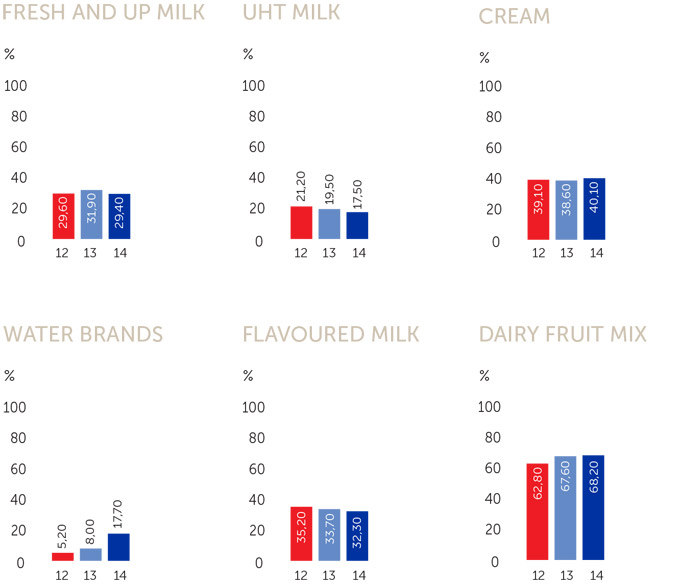

Fresh and Ultra Pasteurised milk

Our market share is 2.5% down against the previous year, while the total market is 2.6% down against the previous year, mainly as a result of aggressive pricing by retailer UHT house brands. Clover’s Ultra Pasteurised (UP) Milk with a shelf-life of 30 days and Clover’s 18 day fresh milk have been well received in the market as a bridge between fresh and long-life milk, buoying volumes and sales in an otherwise tightening market.

UHT milk

As mentioned above, aggressive pricing by retailer house brands saw a 5,3% volume increase in the total UHT market as consumers switched from fresh milk to UHT milk. Clover’s market share in this segment decreased by 2% to 17,5% market share. Clover did not participate in the retailers’ house brand price war.

As a major participant in the UHT market, Clover cannot ignore the market forces which have enticed many traditional fresh milk consumers to switch to UHT. This in turn drove equally aggressive pricing in the fresh milk segment. The combined dynamics are severely curtailing Clover’s ability to put inflationary price increases through and at the same time retain market share.

Cream

Total market volume growth of 4,7% was reported for the year under review and Clover’s market share increased by 1,5% to 40,1%.

Maas

Maas was reintroduced in the second half of the 2013 financial year and experienced good sales volumes which helped the fluids segment achieve overall growth. Clover’s market share in this category increased from 1,9% to 8,1% and the overall market volume growth for Maas was 5,3%.

Feta Cheese

Clover’s own feta cheese market share reduced by 3,6%, but picked up by 6,8% in the Pick n Pay house brand packed by Clover. Overall volume growth for the feta market increased by 4%.

Pure Juices

Overall volumes in the pure fruit juice market decreased by 2,4%. Clover’s market share for its premium Krush brand and Quali Juice brand decreased to 44,9%, down from the prior year’s 46.2% market share.

During the reporting period, a strong migration from Quali pure juice to Quali nectar was noted.

Iced Tea

The Iced Tea segment experienced strong volume growth, up 12,7% on the prior year. Clover successfully addressed supply problems experienced during the move to a new facility.

Through its venture with Nestlé, which came into effect on 1 August 2013, Clover Waters will soon manufacture, distribute, market and sell Nestlé Iced Tea under the Nestea brand in addition to Clover’s Manhattan Iced Tea brand.

The larger entity will compete more efficiently and regain some of its lost market share, which decreased from 28,4% in the previous year to 21.9%.

Dairy Fruit Mix

The overall volumes in the Dairy fruit mix market declined by 9,4% from the prior year. Despite this decline, Clover managed to increase its market share in the Tropika brand to 68,2% against 67,6% in the previous year. This volume decline is mainly due to the price wars in carbonated soft drinks and substitution as a result of the war.

Water

As discussed under Iced Tea above, Clover’s joint venture with Nestlé, Clover Waters manufactures, distributes, markets and sells Nestlé’s Purelife and will add Valvita and Schoonspruit brands in addition to Clover’s Aquartz brand in the future.

The overall market volume for bottled water grew by 8% during the year under review and Clover Waters market share in this segment has grown from 8,0% to 17,70%. This is mainly as a result of the Nestlé Purelife water, that is with effect from 1 August 2013, included in the market share.

Pre-packed cheese

The total pre-packed cheese market grew by 34,9% this year on top of the 30,8% growth of 2013. This is because the traditional bulk cheese market volumes have been replaced by price competitive 800/900 gram bulk pre-packed cheeses. Clover participated in this growth although market share was 6,4% down against the prior year.

Flavoured milk

Market volumes for flavoured milk reduced by 3,3% during the review period. Clover’s Super M brand’s market share, decreased by 1,4% to 32,3%, mainly as a result of aggressive pricing by competitors.

Fruit Drink/Nectar

A marginal overall volume decrease of 0,9% (being the total market) was experienced during the reporting period. Clover’s combined market share decreased by 5,1% during the reporting period as a result of, inter alia, the discontinuation of the Capri-Sun brand.

(All market statistics quoted from Aztec are for the year ending 30 June 2014 for only Shoprite, Checkers, Pick n Pay and Spar and should not necessarily reflect total market representative shares.)

stakeholders

Clover is cognisant of its responsibilities to all stakeholders in order to ensure its long-term viability. The Group therefore engages whenever relevant with its constituency to identify and consider the impact its business has on its stakeholders.

Dividends

The Board targets a dividend cover over the medium term based on headline earnings per share, which is more comparable to the sector within which Clover operates. A progressive dividend policy will be generally applied whereby dividends are maintained or grown at least by the same percentage as the growth in headline earnings per share, until such time as a comparable dividend cover is achieved.

In line with this policy, a dividend of 16 cents per share was declared by the Board on 15 September 2014, which brings the total dividend for the 2013/14 financial year to 32 cents per share which is R58,4 million.

Africa expansion

The weakened local exchange rate has to some extent protected the market from opportunistic imports and conversely had a positive impact on some of our foreign subsidiaries, with especially Botswana performing well with increased revenues on the back of larger volumes as well as exchange rate gains.

Our expansion into selected African markets remains a work in progress and although we remain committed to drive Clover’s entry into new markets, local and immediate opportunities which became available following the termination of our restraint of trade with Danone Southern Africa as referred to in the Chairman’s review took priority during the review period.

Outlook value creation

This outlook value creation incorporates Clover’s short, medium and long-term initiatives.

Short term

Despite some of the most challenging trading conditions in recent history, we will continue to deliver on our targets which include volume and market share growth, the reduction of overall costs, especially in the supply chain.

As demonstrated by the success of our new platforms in difficult economic conditions, the successful execution of our expansion plans for new value-added products and platforms is imperative. This will allow us to leverage our iconic brand and production capacity as well as expanding our business further into sub-Sahara Africa.

The investment over the past few years in new packaging equipment will allow for innovative products and concepts to be introduced over time.

This will however require some investment in the shorter term as the launching of new products, platforms and concepts requires marketing support.

Management will continue to deliver against the Group’s strategy of identifying and consolidating long-term growth opportunities that will ensure a sustainable return on investment.

The discontinuation of the Danone services will have some financial implications on Clover, which will be managed by a combination of reducing costs, replacing some of the lost business with other third party services and Clover’s own growth. However, in the short term there may be a delay in replacing the lost fee income.

For a number of years certain retail groups have indicated that they would like to perform their own distribution services to their own stores, which is currently performed by Clover. If they persist, this could lead to a further loss in fee income for Clover, but could be managed more easily than the exit from the Danone services as the direct costs associated with not servicing an entire channel are easier to eliminate. Where the full costs cannot be eliminated, services will be offered to other third parties, for example in rural areas. Nothing to this effect has happened yet, but there are constant discussions with some retail groups in this regard. Similar to the cessation of services to Danone, there could be a lead-and-lag effect in the short term should this materialise.

Some important initiatives in the year ahead include:

Continued research and development of new products.

Re-entry into the yoghurt and custard market.

Maximising our collaboration with the trade – which is dependent on further IT system development.

Continued focus on safety, health and the environment, especially with regards to emissions, waste and water consumption.

Clover is also actively reducing its environmental footprint. These efforts don’t only relate to our own operations but also extend to our supply chain partners who, by nature of their supply to Clover, have a significant environmental impact.

Medium to long term

Consumer spending is expected to increasingly come under pressure, which along with inflationary cost pressures will see further market consolidation. The executive team is focused on maintaining an optimal balance between short-term profits and achieving longer-term growth opportunities which will sustain and improve Clover’s market position on the sub-continent.

HUMAN CAPITAL

Appreciation

Clover has a very competent and committed Board which is actively involved in setting the strategy and ensuring our long-term sustainability. We want to thank them for all their unselfish support. A special word of thanks goes to Mr. Werner Büchner as Chairman, for his guidance during a challenging year.

I wish to thank all staff and their families for contributing to Clover’s success during the year. There is much hard work ahead, but we can build on a solid foundation with pride.

Clover is nothing without its milk. The commitment and passion of our Milk Producers during this particularly testing period was a cornerstone of support. On behalf of the executive management team, sincere appreciation goes to them.

Our supplier partners continue to play a significant role in our sustainability and success. Your efforts in aligning our objectives and support is much appreciated.

A final word of thanks goes to my executive team. It was a tough year and often called for efforts and inputs beyond the call of duty. We wouldn’t have achieved the targets we set ourselves without the cohesion of a team. I sincerely thank you for your support.

For more information, refer to the Integrated Annual Report as well as the Report on the Six Capitals on www.clover.co.za.

Johann Vorster

Chief Executive

15 September 2014

• Brands

• Corporate Governance / transparency

Market Share