Business review

Chief Executive’s report

Despite the challenges during the year, we remain committed to our medium to long-term goals of investing in and growing our value-added product portfolio and infrastructure.

Despite the challenges during the year, we remain committed to our medium to long-term goals of investing in and growing our value-added product portfolio and infrastructure.

Introduction

Clover faced an exceptionally challenging year as South African food producers and retailers had to contend with several complex and ongoing issues in the economy. I have always maintained that our business has numerous levers at its disposal to mitigate operational risk, and these were certainly tested during the period.

Some impacts such as the prolonged drought, a wetter and cooler summer and rand volatility were beyond our control. The resultant above-inflation input costs, subdued volume growth and continued low consumer spending amidst aggressive competitor pricing meant that we had to take some very tough decisions during the year, to position and sustain the business optimally against a constrained “new reality”.

This obviously came at a price as reflected in our subdued financial performance. The fact that the 2015 and 2016 financial results set an exceptionally high benchmark we were very conscious of guarding against short-term, knee-jerk solutions. We are confident that the measures implemented during this reporting period will not only ensure sustainability and growth during the current downcycle, but will position Clover optimally to take advantage of any economic tailwinds, once the economic tide has turned.

Product group sales volumes for the year contracted in most categories, except for fermented products and deserts, which showed resilience on the back of further capital infrastructure investments to meet demand. Revenue improved by 2,4% or R239,9 million to R10 058,6 million. Sale of products increased by 3,3% to R9 401,8 million, despite overall volume decreases of 3,5 % given the subdued consumer sentiment within the constrained economic climate.

Headline earnings decreased by 65,9% or R235,0 million to R121,6 million. This decrease in headline earnings is primarily because of:

- headline operating profit, which decreased by 52,3% or R298,4 million

- net finance costs, which increased by 18,0% or R20,3 million

- income tax expense which decreased by 63,9% or R72,9 million. The effective tax rate base decreased by 3,9% to 20,6% that is explained in more detail under “Profit for the year” later in this report

- share of profit from a joint venture, which increased by 29,6% or R4,2 million

- non-controlling interests, which decreased by 51,4% or R0,5 million.

Profit attributable to shareholders of Clover Industries Limited declined by R192,6 million.

Following the implementation of several promotional strategies, market shares started recovering significantly since April 2017, as reflected in the graphs below.

In my report, I will elaborate on the strategic structural changes implemented during the reporting period, its expected impacts and leveraging of opportunities. For a complete overview on the business, its performance and prospects, this report should be read in conjunction with the Chairman’s report as well as the Chief Financial Officer’s report.

Financial strategy and operational restructure

Since listing in 2010, we have been working towards diversifying Clover’s business away from low-margin, commoditised bulk dairy products, focusing on higher margin value-added branded food and beverages to improve operating margins across the portfolio. In contrast, profit on traditional dairy products are typically driven by volumes and this would apply to fresh milk, ultra-high temperature milk, ultra-pasteurised milk, skim milk powder, whole milk and bulk cream.

A recent strategic review of our product portfolio highlighted new trends in the milk business model where owner-producers supply the trade directly, as opposed to traditional intermediary companies like Clover. This means that commodity products like fresh, UHT and UP liquid milk (“non-value-added drinking milk”) has drifted outside of our core product portfolio.

Since our strategic focus is on value-added product categories, it made strategic sense to transfer the supply and demand side of the volume driven business to a new entity and invest our future funds in more profitable businesses that will suit our business model better, whilst remaining a substantial service provider to the dairy industry.

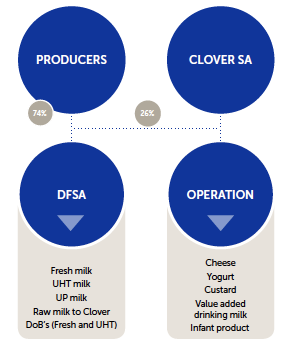

In one of the biggest milestones since Cielo Blu in 2010, we formed a wholly owned subsidiary (called Dairy Farmers of South Africa (Pty) Ltd (“DFSA”)) which houses the non-value added dairy business of Clover with effect from 1 April 2017. DFSA is responsible for the procurement of raw milk as well as the selling, marketing and distribution of the non-value-added drinking milk above.

DFSA will still supply all of Clover's milk requirements as long as it can guarantee supply at competitive prices. It is important to note that Clover’s Unique Milk Procurement System (CUMPS) aimed at balancing Clover’s raw milk intake with expected dairy sales, will remain in its current format.

In practical terms, this means that DFSA will source and supply Clover with its milk requirements, including (but not limited to) final product to the trade and other customers, exports, house brands, etc. Its scope will be limited to drinking milk (fresh, UHT and UP milk), bulk cream and milk powders under the Clover brand or other own brands, various Dealer Own Brands (“DOB’s”) and the selling of raw milk to Clover.

In terms of the transfer agreement, Clover holds all the A shares in the new business with 26% voting rights, whilst the milk producers hold all the B shares with a 74% voting right.

It is envisaged that Clover will buy most/all of its milk requirements from DFSA. All existing Clover producers will therefore still supply all of Clover’s milk requirements.

Clover has leveraged the high-volume and short shelf-life characteristics of some of the commodity dairy products to drive its expansive chilled distribution chain, as the carrier not only for its own value-added products but also for its principal distribution business. DFSA will subsequently become Clover’s largest principal, where all its related requirements such as distribution, production, administration (invoicing, debt collection, marketing), IT services, payroll administration, central services, sales and merchandising are outsourced to Clover for an initial period of 20 years.

To Clover, this means that we will continue to focus on:

- Promoting and developing value added products in dairy and other related food categories;

- Expanding its non-alcoholic beverages portfolio; and

- Developing and enhancing its key competencies in brand development, production distribution and merchandising.

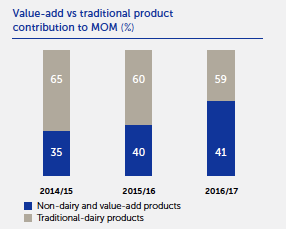

Core portfolio vs non-core portfolio (volume driven) growth

A key measure of the impact that our focus on value added and non-dairy product volume have is reflected in the Margin on Material (MOM).

During the reporting period, the overall MOM of non-alcoholic beverages, fermented products and desserts and other value-added products increased from 53% to 54%. The restructure and formation of DFSA is expected to impact this ratio significantly going forward.

Stringent cost saving initiatives in a high cost inflationary environment

The raw milk supply was volatile during the reporting period which followed the prolonged drought. Seasonal peak milk production commenced in August 2016 with high feed costs placing downwards pressure on milk production whilst industry selling prices remained relatively low. The drought in the Highveld and Kwazulu-Natal was subdued with great summer rainfall, while the sub-optimal conditions in the Western and Eastern Cape prevailed. The country’s milk flow was relatively stable when compared to the prior year, but the cooler and wetter summer in December 2016, and the higher selling prices, resulted in volumes decreasing, particularly in the beverage segment.

Significant once-off restructuring costs of R48.1 million relating, inter alia, to the integration of the City Deep distribution facility into the Clayville distribution facility, the closure of our Upington and Kimberley distribution centres and the mothballing of our Bethlehem powder facility were incurred during the current year, that will bode well for future cost efficiencies.

On the back of current market conditions, we focused on cost saving drives during the review period, with the management team driving efficiencies and cost savings, especially on variable costs, exceptionally hard. Executive management volunteered for a salary freeze. Head office managed to avoid inflationary increases to overheads and reduced its overall spend by 9,6% or R25,0 million.

Strategic Capex spend

Despite the challenges during the year, we remained committed to our medium to long-term goals of investing in and growing our value-added product portfolio and infrastructure. We also continued to explore synergistic opportunities to leverage infrastructure that will result in significant cost savings that can be passed on to consumers.

Project Sencillo was launched during the year, which involves optimising capacities and increasing efficiencies. It will mean moving equipment around to factories within the group to optimise each factory according to demand and length of production runs, better matching the raw materials and by-products.

Other strategic projects underway include:

- Increasing our distribution reach into previously under- and unserved areas, increasing our delivery points at the bottom-end of the market to 30 000;

- The launch of several exciting new products and line extensions during the next few months.

In the rest of Africa, operations in Mozambique are running smoothly and we are very excited to have launched a selected product portfolio in Tanzania in August 2017.

Cash Flow

Cash generation was constrained given the muted consumer sentiment, and income was therefore also subdued.

Return on Equity (ROE)

Return on Equity is a paramount performance measure for several capital market investors. Throughout the year, we engaged with these shareholders to integrate greater focus on this measure into the long-term incentives for especially senior management. (Refer to the Report on Remuneration, and especially the letter to shareholders on page 78 of this Integrated Annual Report.) Given a stagnant selling price environment, loss of volumes, and above inflationary increases in variable costs during the reporting year, Clover reported a decrease in ROE from 12,9 to 5,5%.

Governance

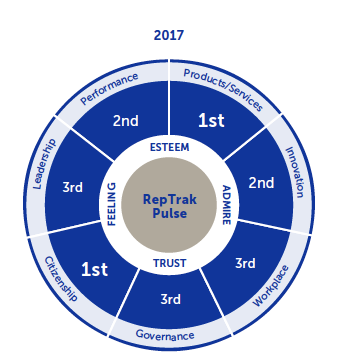

I am delighted to announce that Clover took top honours yet again in the 2017 SA RepTrak Pulse reputation survey as “the most reputable company on South Africa.” Seven out of the top 10 winners are FMCG or retail companies, showing the importance of consistent delivery of quality and product to the market on reputation and trust.

Clover placed first in Citizenship and first in Products and Services which is an outstanding demonstration of the organisation’s resilience and adaptability. We pride ourselves on being a mature organisation, applying global best practice through an Enterprise Wide Risk Management Framework.

The Board and management views corporate governance as paramount to sustainability and our risk policy and framework incorporate guidelines by The Committee of Sponsoring Organisations (COSO).

Human Capital

The Reptrak study mentioned above refers to Clover’s ranking as “an ideal company to work for.” This accolade is supported by our exceptionally low staff turnover and high-performance culture. As a management team, we go to great lengths to ensure staff across all levels in the organisation is well-informed of our objectives and the strategies to achieve this.

Establishing a “creative tension” drives our strategy and “Way Better” philosophy, retaining key skills within the business, such as with the City Deep facility integration into Clayville, where most staff were redeployed in the business. The Board subscribes to and supports Government’s equity objectives and broad-based black economic empowerment. To this end we work closely with Government to unlock opportunities, such as our Masakhane project, that has already created a significant number of permanent employment opportunities and is set to create hundreds more.

More information on Masakhane and other Human Capital initiatives can be found here and here of this Integrated Annual Report.

Natural Capital

Agriculture generally experience cyclicality, with dairy being no different. Although the resultant high- and low flow of raw milk during seasonal cyclicality can be planned for, external impacts such as weather patterns, input cost increases such as fuel, fertilizer and feed have dramatic effects on the sustainability of the primary industry. Growth in dairy consumption strongly correlates with GDP growth, and in a low- to no-growth economy such is currently the case in South Africa, there is little chance to recover these costs through increased volumes.

During the review period, Clover increased the price it paid to dairy farmers to ensure the sustainability of the primary market.

Producers will set market prices for the non-value-added drinking milk in the different category segments. Clover will in turn purchase raw milk from DFSA at the average national milk cost (including milk price, collection, inter-branch-and handling costs) for all its other products containing milk (cheese, yoghurt, custard and the like). In this way, DFSA and its producers will still participate in the full value chain of value added products, our raw milk source remains secure in the face of all foreseeable eventualities and we anticipate that the improved weather conditions forecasted for 2017 will normalise milk production.

The aim of the DFSA structure and the Clover Unique Milk Procurement System (“CUMPS”) is to protect the primary industry in South Africa as dairy producers have control over pricing and greater see-through on potential milk offtake. The irony is that South Africa produces some of the highest quality milk internationally. Production capacity is not the challenge – finding a sustainable offset point for this production capacity is, but I will elaborate more on that under Manufactured Capital below. The sustainability of Natural Capital is recognised throughout our value chain, including our carbon footprint, electricity consumption and wastage. Readers should refer to the chapter on Natural Capital here of this Integrated Annual Report for more information.

Manufactured Capital

Over the past two financial years we invested heavily in our production infrastructure. Considering the strategic review during the year and our position that muted consumer demand will continue, infrastructure capacity will be consolidated into the most optimal facilities through project Sencillo. Capital expenditure has furthermore been reduced significantly in comparison with prior years. A longer-term ambition is to pragmatically centralise all our major production facilities into a strategically located and purpose-built industrial park strategically located near supply sources, other production facilities and major transportation routes.

Intellectual Capital

The hyper competitive retail industry is moving towards planning its product selection and stocking levels through an average daily rate of sale, whereby future customer orders will be calculated by a statistical algorithm and the retailers themselves take hands-on control of their demand and in-store planning. Clover’s leadership decided on an aggressive approach to evaluating and adopting technologies that will future-proof Clover. To this end we have partnered with IBM to develop a proprietary business intelligence system to support management decision-making at all levels. This “Kolabo” project will enable managers to use “big data” analysis for insights into market dynamics, trends in consumer consumption and the needs of our clients.

The Group therefore continued to invest in considerable new IT collaboration infrastructure to enhance sales.

The largest component of Intellectual Capital is our brands, the performance of which is outlined below. All the market shares and market growth statistics discussed below are based on the independent “Nielsen Total Trade Desk” data (“Nielsen data”), which comprises Shoprite Checkers, Pick n Pay, Woolworths, Spar group and Fruit and Veg City data and is consistent with the measures applied in prior reporting years. It is important to note that our Masakhane initiative does not form part of this data (If included, Masakhane would have had an influence on the value-added products’ market shares, since we are taking our most important brands and products closer to the people at much better margins since there are no trading term costs, returns, etc).

Going forward, Clover will only report market shares for its value-added brands and not for the brands sold under license by DFSA.

Fresh and ultra-pasteurised milk

Clover’s volume only decreased by 8,4% against the prior year, mainly because of aggressive retail house brand pricing of UHT stock and low volumes of milk flow. The total market for fresh milk contracted by 3,9% against the comparative year also reflecting the pricing strategy of retailers and general lacklustre consumer demand.

UHT milk

Continued aggressive pricing resulted in overall total market volume growth of 4,6% for Clover (including DOB production), that was better than the 1,0% market decline recorded in the industry. During the current year, Clover’s UHT volumes in the Nielsen channels also contracted because of Clover’s increased involvement in Dealer Owned Brands, Clover’s market share contracted from 14,6% to 14.1 % for the year.

Cream

Total market volume growth expanded 0,4 % for the year under review. Because of lower fresh milk sales, Clover’s volumes contracted by 6,3%.

Maas

Clover’s volumes grew by 6,0% and we continued making inroads into this segment by growing market shares from 9,3% to 9,6%

Feta cheese

Clover’s volumes declined 5,3% on the back of a market increase of 0,3% primarily because of higher selling prices.

Pure juices

Overall volumes in the pure fruit juice market continued to decrease, reflective of reduced discretionary consumer spend, price increases to recover significantly higher input costs and an unusually wet and cold summer season. Despite a contraction in the overall market 6,8%, Clover’s volumes decreased 4,8%, but its market share in the top-end grew from 42,9% to 44,3%.

Iced-tea – ready to drink

The ice tea category continued to lose market share from 17,2% to 15,1% because the rainy and cooler summer impacted sales. Clover’s volumes decreased 24,6% and this competitive category also decreased 8,8% in the top-end.

Dairy fruit mix

Clover grew its market share from 79,0% to 83,9% through its popular “Tropika” and “Danao” brands. Given higher pricing and the adverse weather conditions during the festive season, volumes decreased 3,8% in this category. The launch of Clover’s new Tropika Slenda with less sugar has been very well received in the market.

Bottled water

The total market volume in this segment increased by 10,7% during the year under review although Clover Waters’ market share in this segment declined from 11,0% to 7,3%, mainly because of strong competition.

Pre-packed cheese

The overall volumes for natural pre-packed cheese declined 25,1% during the year under review. Clover’s market share in this category (in the top-end) however grew from 17,0% to 18,5% as certain volumes in the prior year was sold in bulk.

Flavoured milk

Clover’s “Super M” brands volumes decreased by 6.6%, and its market share grew from 29,7% to 31,9%.

Yoghurt

Clover entered the yoghurt category in January 2015 by introducing its own range of yoghurts under “The Classic” brand, in addition to the manufacturing and distribution of the acquired and relaunched “Fruits of the Forest” brand.

Clover volumes grew by 5,3% during the year under review, following the commissioning of additional capacity to address consumer demand. Clover’s market share for the year grew from 8,3% to 8,7%.

Custard

Similar to yoghurt, Clover only entered the custard market in January 2015. Volumes in this market category declined 1,5% and Clover’s share of this market’s annual sales volumes was 10,1% compared to 7,6% previously. Clover’s total volumes grew 31,7% in this category.

Butter

Total market volumes contracted by 5,4% because of low inventory levels and the availability of cream. Clover’s volumes declined 19,5%, and market share decreased from 29,9% to 28,0%.

Other

Olive oil and soya products performed in line with expectations off a low base.

Social and Relationship Capital

Winning the SA RepTrak Pulse reputation survey as the most reputable company in South Africa for the second consecutive year is a great honour and achievement that every Cloverite feels exceptionally proud of.

In addition to this, the Clover Mama Afrika project launched in 2004 is close to my heart, being such a practical and authentic means of channelling self-empowerment, skills development and dignity into marginalised communities. This worthy undertaking was again recognised by winning PMR’s prestigious Diamond Arrow Award.

Outlook

At the turn of the century, some members of the current senior executive team played an instrumental role in initiating far reaching changes in Clover’s business model, converting it from a dairy co-operative to a demand driven manufacturer and distributor of branded food and beverages.

Our vision for Clover has always been much more long-term than any particular market cycle. We therefore remain optimistic and excited about Clover’s future as we have considered and employed measurable strategies that will return the Company’s profitability to historic levels over the medium and longer term.

As a team, we will increase volumes and claw back market share by passing cost efficiency gains on to the consumer. I still maintain that the secondary industry is too fragmented, creating unnecessary costs in the manufacturing and supply chain. We will continue to leverage our asset base and infrastructure as we grow our core portfolio of value-added branded products.

Aligned with our strategy to expand our value-added portfolio and to support future cost efficiencies and increased sales, we made significant investments into our production facilities, distribution platform, research and development as well as marketing during the reporting period. We are confident that the benefits of these investments will create a platform for adjacent plays and future growth.

The exploration of adjacent revenue streams is a key focus area along with further investment in research and development of new differentiating products which may be implemented in-house or in collaboration with industry counterparts. Despite the difficult operating environment, Clover remains committed to our medium to long-term goals of investing in and growing our value-added product portfolio and infrastructure.

The weakened economy will continue to take its toll on consumers whilst we address the challenges of above inflationary cost increases. We are acutely aware of the plight of the consumer and remain focused on seeking cost efficiencies and more affordable products across our value chain as this will limit the impact of rising selling prices and defend our market shares. We will continue to explore opportunities where synergies can be leveraged using our infrastructure. This should lead to significant cost savings which can be passed on to the consumer.

At the time of writing, the implementation of DFSA has progressed well and the company has taken some proactive steps in addressing the expected undersupply of raw milk in the coming season. In addition, some innovative incentives were introduced to stimulate the production of butterfat and address the butter shortage in South Africa.

Clover’s executive team has set high but achievable targets for the year ahead. Each executive member recently committed to the following five habitual behavioural attributes to drive value:

- Consumer centric – Lower cost, better prices, better offerings.

- Cost focus – Challenging all cost to unlock fuel for growth in adjacent categories.

- Ambitious – Achieving ambitious and clearly defined financial targets.

- Responsive and flexible – Responding to market challenges through quick responses and decisive actions.

- Supportive – Create a culture of acting as one and reaching goals together (the core business)

Several actions implemented during the latter part of the reporting period started yielding encouraging results, the impact of which is expected to reflect in the interim results for the current financial year and beyond. Some of these milestones are:

- The unbundling of DFSA as a separate entity, eliminating further exposure to the cyclicality of the non-value-added drinking milk market

- Material changes to a number or recipes in our products that produced cost savings and lower cane sugar content

- Significant cost savings across the board for the new budget year

- Project Sencillo well underway (optimising factories and simplify operations across the manufacturing value chain)

- The drought has abated, and volumes are being restored with a bumper maize crop expecting to reduce feed cost in some areas

- Market shares are starting to return to normal levels

- Recent new product launches starting to pay off - albeit off a low base

- A number of product showing increased gross margins, e.g. fermented products, dealer own brands, etc

- Addressing any material tax impact on products containing sugar

- New product launches well under way

- Masakhane roll-out accelerated

Appreciation

I would like to thank the Board, especially Mr Werner Büchner, for its continued support and guidance during a challenging 12 months.

I would like to thank the Board, especially Mr Werner Büchner, for its continued support and guidance during a challenging 12 months.

Our relationship with our producers remain a beachhead for our sustainability and once again I thank them for their continued support and interaction.

Mr. Elton Bosch decided to pursue personal interests and will leave the Company in December 2017, after a handover process to a new incumbent. Elton, it was a pleasure working with you and I thank you for your contributions, support and input, not only during your tenure as Chief Financial Officer, but your time on exco as well.

I want to thank each staff member and their families for their devotion and hard work during a challenging year – your “Way Better” approach to challenges has carried us through.

Lastly, a final word goes to my executive team for their hard work and commitment.

Johann Vorster

Chief Executive

11 September 2017

All market shares shown here are based on data received from Nielsen. Please note some market shares for 2015 have been restated due to changes made in the Nielsen database.

Please click on the images to see enlarged versions.